Through a series of moves, the Reserve Bank of India (RBI) has intensified its scrutiny of the credit card industry. Recently, it asked Federal Bank and South Indian Bank to stop issuing new co-branded credit cards, reportedly concerned about the access their fintech partner, OneCard, had to customer data. Earlier this year, the central bank came down heavily on Paytm for not complying with its rules related to KYC and data sharing with non-regulated entities, effectively shutting down its payments bank. This also highlighted RBI’s concerns about digital lending. Its recent move on co-branded cards showed that credit cards are also on its radar.

In November 2023, the RBI increased the risk weightage for credit cards from 125% to 150%, effectively increasing the minimum amount of capital that banks have to hold to cover the credit risk from the instrument. Responding to an RTI query by The Indian Express last year, the RBI said that defaults in credit cards were at 2.2% of the total outstanding amount in April-December 2022.

However, banks’ exposure to credit cards has expanded aggressively, growing 31% in each of the last two annual periods to January, according to RBI data. This was the highest among nine retail lending segments in the 2022-23 period and the second-highest in the 2023-24 period.

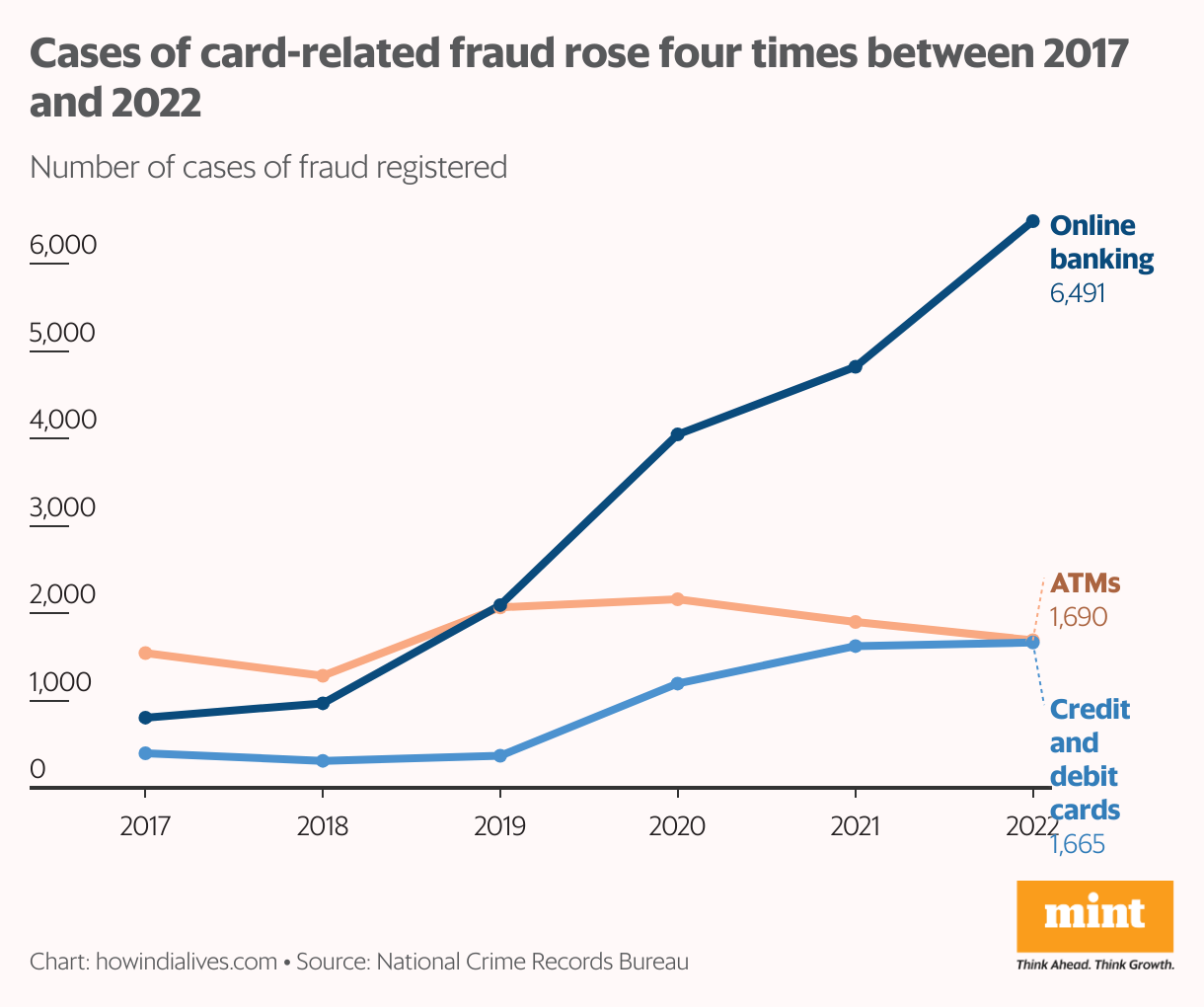

RBI has also been concerned about growing fraud. It’s a reason why it cracked down on digital lending earlier and took action against entities that were lax on KYC norms. Both online and card-related frauds have jumped in recent years, according to the National Crime Records Bureau.

Commercial concerns

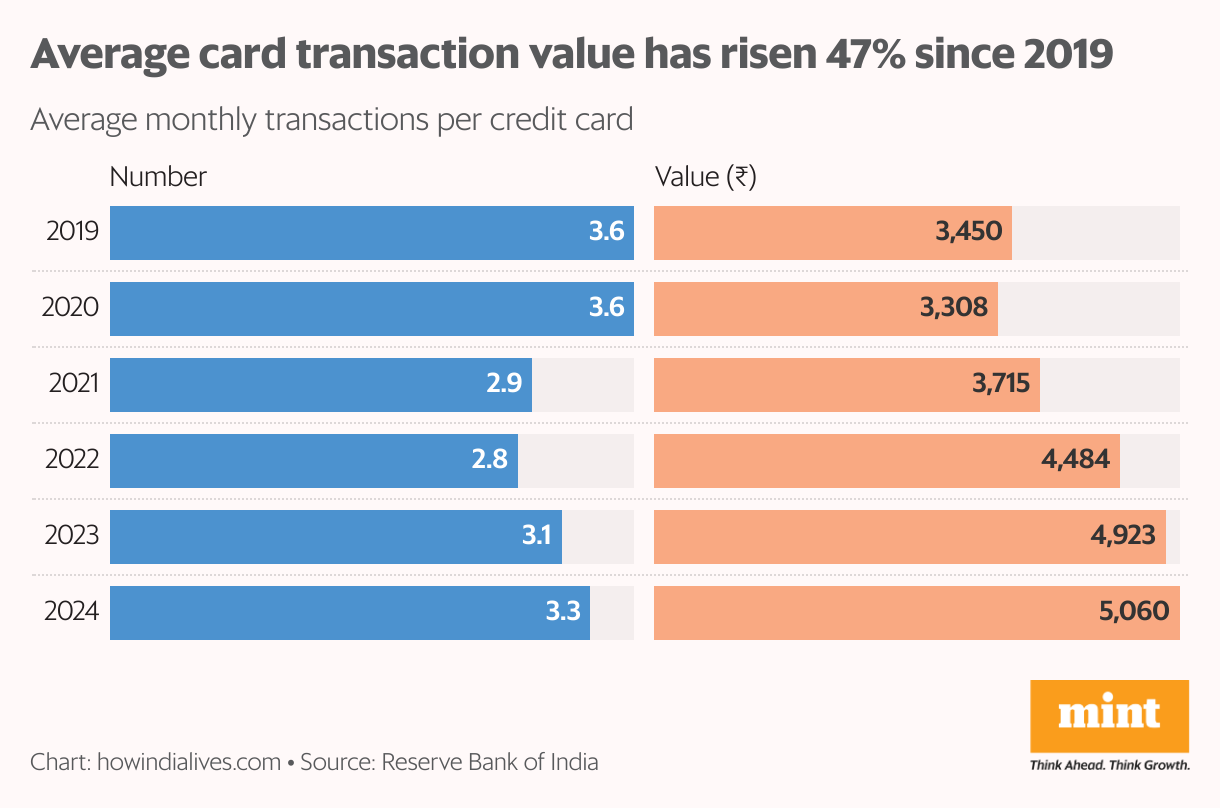

The number of outstanding credit cards has more than doubled since 2019. While the number of average monthly transactions per card has remained stable between January 2019 and January 2024, at about three transactions per card, the average value has grown by 47% during this period to about ₹5,000 in January 2024.

While a number of reasons are driving this growth in transaction value, one has come under RBI scrutiny: commercial cards. Last month, it ordered Visa, a major global network that enables credit card transactions, to pause payments by corporations to other businesses through commercial cards. Companies use this system as a way to get interest-free credit. Last month, Mint reported that commercial cards accounted for a fourth of all credit card spending. The regulator was concerned that some fintech companies, which act as intermediaries in these transactions, might be violating the Payment System Settlement (PSS) Act.

Co-branded boom

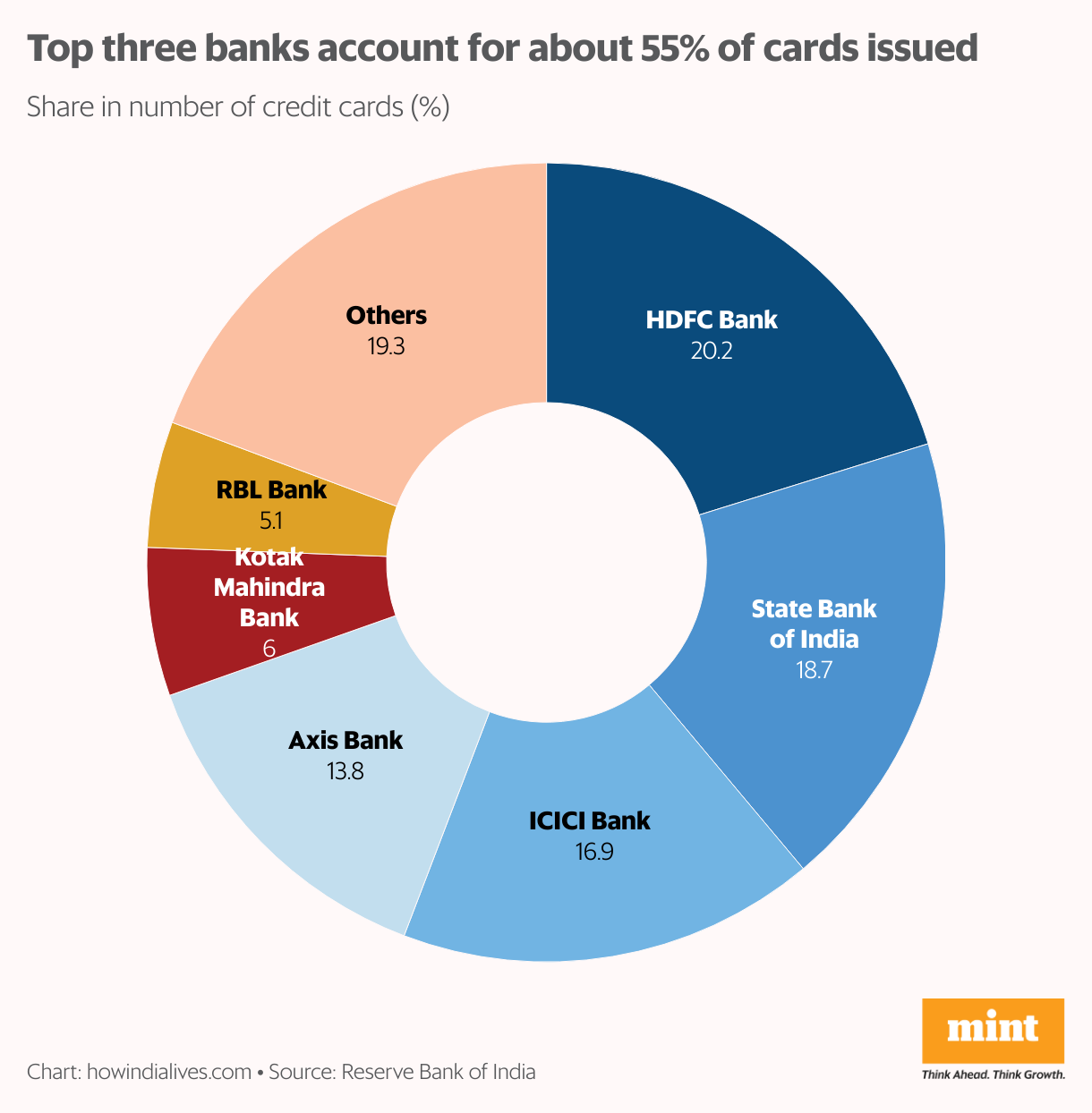

The top three players in the Indian credit card market are HDFC Bank, State Bank of India and ICICI Bank. They account for about 55% of cards issued, leveraging their brand recognition and networks. The size of the market by number of cards grew 20% between January 2023 and January 2024, with little change in their ranking.

The co-branded cards segment was one growth driver. In a January report, fintech Bank Bazaar called co-branded credit cards “the flavour of the season”, as banks partnered with merchants and platforms to access a bigger pool of customers, especially the younger and tech-savvy ones. In the co-branded segment too, the big three players had an advantage, tying up with well-known brands. For example, HDFC has a partnership with Swiggy, SBI with Air India, and ICICI with Amazon. Meanwhile, fintechs were also hoping to build their brands, often getting into a grey area.

Changing landscape

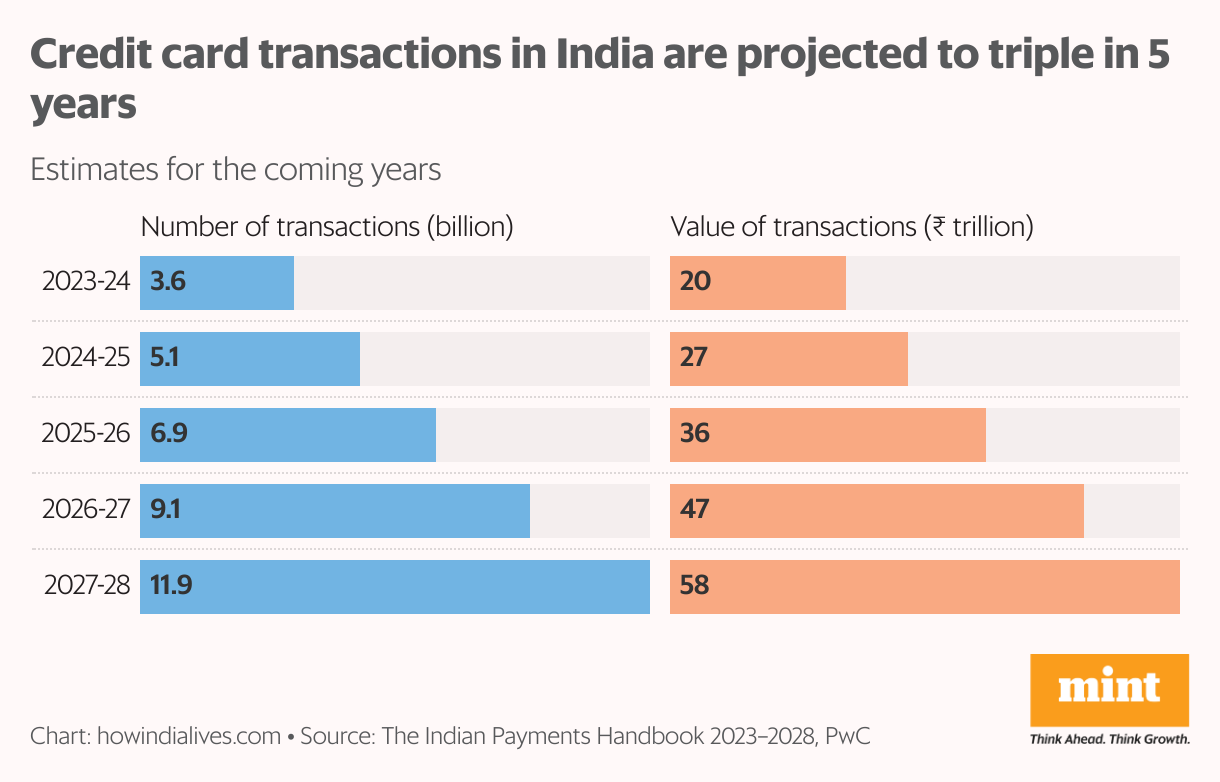

Last year, consulting firm PwC projected an increase in credit card transactions in India from 3.6 billion in 2023-24 to 11.9 billion in 2027-28—or, an average annual growth of 35%. In value terms, it pegged growth at 30%. It will be a continuation of a trend driven by “the availability of a 30-45 days interest-free credit period and other features, including cashback and reward points”, PwC said.

However, growth could be tempered by the greater regulatory scrutiny. For example, earlier this month, the RBI issued a circular on credit card network portability, requiring banks and card issuers to enable customers to choose their preferred network (Visa, Mastercard, Rupay, etc). In recent years, the regulator has taken an open but cautious approach towards fintech, and technology in general. Its recent stand on Federal Bank and South Indian Bank is a reflection of that.

www.howindialives.com is a database and search engine for public data.