India’s life insurance industry has come together to bridge the high protection gap—the difference between available insurance cover and actual needs in case of a policyholder ‘s death— by organizing awareness campaigns and offering more flexibility to customers in terms of coverage and mode of payment. In an interview with Mint, Mahesh Balasubramanian, managing director, Kotak Mahindra Life Insurance, says reinsurance support and additional health data of consumers that helps reduce friction around underwriting are equally important to increase protection in the country. Balasubramanian,who says that life insurers should start selling health plans, also talked about composite licence, individual risk-profiling, Bima Sugam and fraud prevention.

Edited excerpts from the interview:

How can awareness around term insurance plans be increased, given that the life insurance protection gap in India is 87%, as per a recent study by National Insurance Academy?

The industry needs to come together and start awareness campaigns where protection is a key theme so that customers can understand products and natural demand gets created and met. From a product availability perspective, it is quite adequate along with the flexibility at the customer level. Sachet products are available where insurance can be bought at minimal premium. Premium payments can happen monthly, quarterly or annually while policy can be bought for one, two or even five years in one go. Return of premium plans are popular because it caters to the customer segment which wants something back in case they survive the policy period. Our recently launched product Kotak TULIP is also aimed at providing high sum-assured to customers along with market-linked returns.

What we also need to do is reduce the friction around underwriting and increase the capacity from the reinsurer’s side. So, better presence, products and awareness, and reducing the friction to purchase insurance are all enablers for the industry to focus far more on protection.

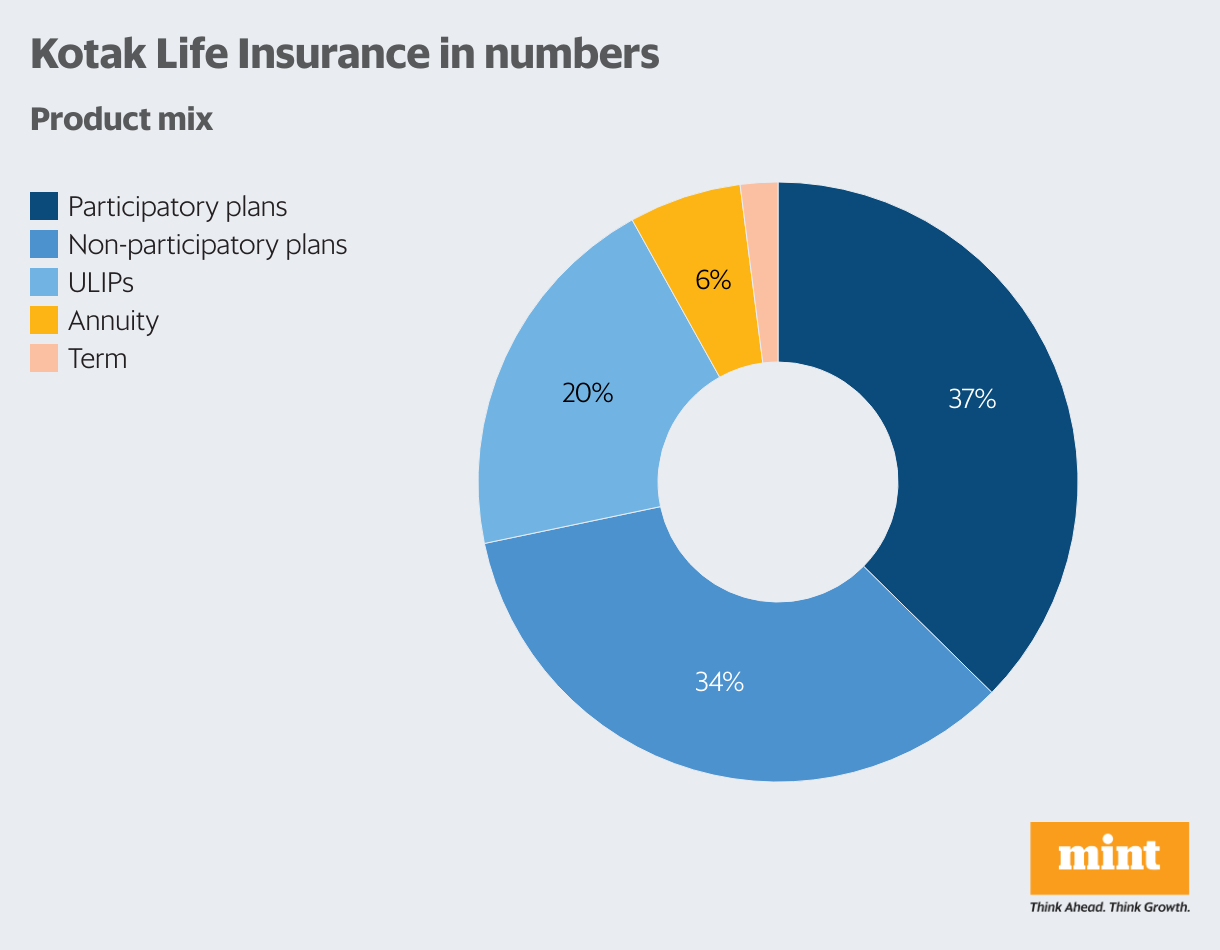

View Full Image

What is your outlook on composite licence? Should life insurance companies be allowed to sell health plans?

It has two aspects. One, everybody can do everything. It is certainly a solution to low penetration of insurance but we have to wait and watch as to when the regulations will be amended and implemented. A near-term solution can be worked out. Instead of manufacturing health plans, life insurers can at least be permitted to start selling it. We need to understand that insurance agent attrition is real. Their viability is not improving because the average commission does not suffice their decent sustenance. If they can offer more products to the same set of customers of the same or a complementary brand, it will help them meet their viability. So we should definitely allow distribution of health insurance products by life insurance companies.

What is the latest update on the IRDAI’s proposal of increasing the surrender value for policyholders? What is your stance on it?

The industry has taken time till January-end to respond to the proposal. The Life Insurance Council, which consists of all the players in the life insurance sector, is compiling responses. While it is good that customers can get better surrender value, the entire concept needs to be understood from multiple angles—from products to risk management. A whole lot of things are there. The council will send its recommendations to the regulator.

What measures are you taking to increase insurance penetration in rural India? The latest Irdai report shows insurance penetration reduced from 3.2% to 3% in FY23.

The insurance industry is trying to design a combined product bouquet being offered to rural India at ticket sizes easily taken by them and in multiple units. This product will have a combination of life, non-life and basic fire insurance, etc. It will be a package of insurance which meets basic insurance requirements of a customer across all product categories of what insurance companies can offer. Once the Bima trinity (Bima Sugam, Bima Vistaar, Bima Vahak) comes in, it will propel the reach of insurance. The implementation is not too far away. It will be a game changer.

Apart from insurers, brokers, agents and other ecosystem players such as UIDAI, Insurance Information Bureau (IIB) and credit bureaus will also join the platform. So wherever data is available, the idea is to build APIs and leverage on the data to get adequate information about the customer so that we can service the customer better. It will essentially be a gigantic platform where the entire fraternity which caters to insurance in various forms and shapes will all be available on a single platform. Of course the products and services that we offer will all be curated, and will be expanded over a period of time. One can’t say that everything will be available on day one. The idea is to make sure that the basic stuff is available and all the players in the ecosystem start participating.

In state level insurance, all insurers have been assigned states to work on insurance penetration. They’re all talking to their respective state governments to popularize these products. The insurance industry is happy to embrace the entire account aggregator framework also. One needs to see to what extent the account aggregator framework succeeds in terms of having more customers enrolled and all the banks providing more and more information after a customer’s consent. Over the next couple of years, you will definitely see a remarkable improvement in the penetration of insurance products in rural India as these initiatives get off the ground.

What is the industry doing to create a centralized database for risk management and prevent fraud?

The typical frauds which keep happening are substandard lives entering our system and immediately lodging a claim. Insurance is a probability industry. We can’t battle against somebody who’s coming in with certainty that he is going to die in three or six months. Usurious entities are getting created. There are so many cases where a person’s entire entity has been faked. All of us are working with the insurance information bureau (IIB) and other data repositories where we are able to go and check fraudsters. The way credit bureaus provide credit scores, insurable scores can also be calculated. We just need more data. Bima Sugam is a solution to frauds also. Once we reduce frauds, the benefit will be passed on to consumers.

The Irdai chief has talked about having an individual risk-profiling in premiums and not the group average. How will it be done?

It is like having a personal designer. We need a lot of information for individual risk-profiling such as demographics data, the customer’s lifestyle, his other purchases. Where is he working? What is his income? How many children does he have? What are the existing policies that he has? The more information we have about the customer, the better underwriting that can be done and customized products offered. For example, if you have never had a health claim for the last 10 years, it means I’m dealing with a healthy life. If you are participating in marathons, that information tells me a lot about your health. We already have a dynamic risk model in which we score customers on different parameters. For now, we use it to seek additional information for underwriting, but tomorrow it can be used for individual risk profiling.